Advertisement

CRM FanzineFaves – The best CRM for banking and wealth management in 2026 must unify the entire client lifecycle, integrating portfolio management, KYC processes, and digital onboarding into a single ecosystem. Top-tier solutions must prioritize explainable AI to satisfy regulatory scrutiny and support complex, multi-generational family structures rather than simple contact management.

DynaTech Systems reports that companies can achieve a return on investment (ROI) of $8 for every $1 spent on CRM implementation.

How do you prevent a CRM implementation failure in high-compliance finance?

To prevent CRM failure, firms should adopt a Preventive CRM Maintenance Routine. This technical workflow includes daily monitoring of integration health dashboards, weekly duplicate detection scans, and monthly full system health checks.

Advertisement

The Data Silo Trap

A primary failure mode occurs when firms implement multiple integrated systems instead of a unified platform, leading to fragmented client profiles. When an advisor cannot access a single source of truth, the risk of compliance failure increases exponentially. This fragmentation often results in digital transformation failure because the technology fails to support actual growth goals.

Avoiding Black-Box Compliance Risks

In the high-stakes environment of 2026, relying on unverified algorithmic outputs is a recipe for disaster. If an AI suggests a portfolio shift without a visible reasoning trail, it creates “compliance drift.” To mitigate this, firms should adopt a Preventive CRM Maintenance Routine, which includes daily monitoring of integration health dashboards and monthly full system health checks.

The Integration Stress Test: API Latency and Circuit Breakers

CRM integration challenges require deep technical knowledge and financial services expertise to avoid system-wide crashes. High-performing implementations must utilize automated alerting and circuit breakers to manage API latency. Without these, a single slow connection to a core banking system can stall the entire advisor workflow. For example, a failure to implement retry logic during a high-volume period can lead to significant data loss during client onboarding.

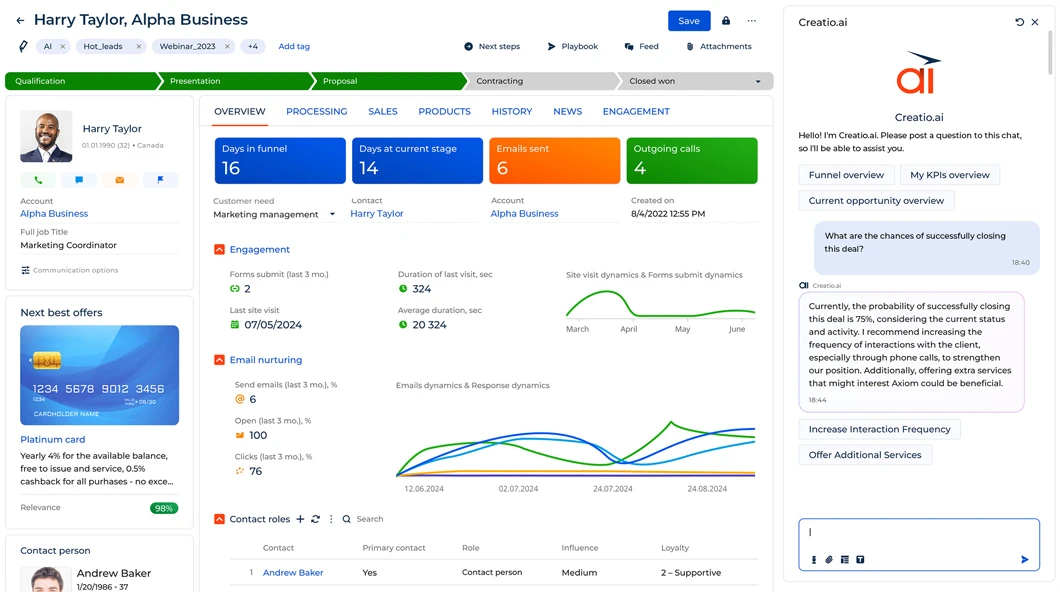

Is your CRM AI ‘Explainable’ or a ‘Black Box’ risk?

In 2026, wealth management AI must be explainable and auditable. Regulators increasingly scrutinize algorithmic decisions; therefore, ‘black box’ AI recommendations that lack clear reasoning trails pose significant compliance risks and will not survive regulatory reviews.

InvestGlass has noted that “Black box AI recommendations won’t survive compliance reviews.” This is because the 2026 regulatory landscape demands that every automated suggestion—from tax-loss harvesting to asset reallocation—can be traced back to specific client data points and market variables. If your CRM uses Predictive AI Targeting to identify high-value clients based on shifts in net worth, the logic must be transparent to auditors.

Shortcut: To audit an AI decision, navigate to Settings > AI Audit Logs > Decision Traceability to view the specific data inputs used for a recommendation.

The AI Auditability Framework

Effective wealth management frameworks must utilize Predictive AI Targeting. By analyzing shifts in net worth, career stage, and life event signals, the system identifies high-value prospects. This provides a clear “why” for every alert generated.

Next Best Action vs. Next Best Client Models

Firms must choose between two distinct methodologies. Next Best Action models focus on optimizing current interactions with existing clients to increase retention. Conversely, Next Best Client models use predictive intelligence to identify future high-value prospects. While the former stabilizes your current AUM (Assets Under Management), the latter drives aggressive growth by targeting heirs and high-net-worth individuals before they enter the market.

Which CRM is best for your specific financial scale?

Selection depends on firm size: Wealthbox and Redtail are optimized for small advisory practices, while Salesforce Financial Services Cloud and Oracle serve large-scale retail and corporate banking. For specialized automation, LendSaaS and InvestGlass offer niche-specific workflows.

Wealthbox and Redtail provide essential features for RIAs and small advisors. While these tools manage core client needs, they may hit scalability ceilings for multi-jurisdictional managers handling massive, complex family offices.

CRM Entity |

Primary Target Segment |

Key Differentiation |

Est. 2026 Pricing (per user/mo) |

|---|---|---|---|

Wealthbox |

RIAs & Small Advisors |

Advisor-focused UX |

$59 |

Redtail CRM |

Financial Advisory Firms |

Industry-specific workflows |

$39 |

Salesforce FSC |

Large Banks & Insurers |

Massive ecosystem/scale |

Custom |

Pipedrive |

Small Advisory Teams |

Sales-centric tools |

$49 |

InvestGlass |

Wealth Managers/Banks |

Swiss-built automation |

Custom |

Zoho CRM |

General Financial Services |

Horizontal adaptability |

Custom |

The table above illustrates the pricing and segmentation divide between boutique tools and enterprise platforms. While Pipedrive offers a lower entry point at $49 per user/month, it lacks the deep wealth-specific compliance features found in InvestGlass or Salesforce.

Small Advisory & RIA Solutions

For independent advisors, simplicity is a feature, not a bug. Tools like Wealthbox focus on reducing the administrative burden so advisors can spend more time on client relationships. These platforms are designed to handle the core needs of an RIA without requiring a dedicated IT department to manage updates or integrations.

Enterprise-Grade Banking Platforms

Large-scale retail and corporate banking institutions require the heavy lifting provided by Oracle or Salesforce Financial Services Cloud. These systems are built to handle millions of transactions and complex regulatory requirements across multiple borders. They provide the depth needed for institutional-grade security and massive data processing.

Niche Automation: MCA and Wealth Management

Specialized needs require specialized software. For example, LendSaaS provides a dedicated MCA CRM platform designed specifically to automate the funding process. Similarly, InvestGlass offers a Swiss-built, Swiss-hosted platform that prioritizes the high security and automation standards required by global wealth managers.

What is the true Total Cost of Ownership (TCO) in 2026?

Beyond licensing fees like Redtail ($39/user/month) or Wealthbox ($59/user/month), TCO includes data migration, specialized training, and regulatory auditing tools. A successful implementation should target an $8 ROI for every $1 spent.

Financial leaders must look past the monthly subscription to understand the full budget. The sticker price typically represents only a fraction of the total investment required for a successful rollout.

- Data Migration and Cleaning: Moving “dirty” data from legacy core banking systems into a modern CRM is a massive undertaking. Without rigorous cleaning, the new CRM will immediately suffer from duplicate records and inaccurate client histories.

- Integration Maintenance: Maintaining API connections between the CRM and external portfolio management tools requires ongoing technical oversight.

- Regulatory Auditing Tools: In 2026, you must pay for the ability to prove your AI is compliant. This includes the cost of specialized auditing software and the man-hours required for compliance reviews.

- Staff Training: A CRM is only as good as the people using it. If advisors find the interface cumbersome, they will revert to spreadsheets, rendering the investment useless.

When calculating ROI, remember that the $8 return per $1 spent is achieved through increased productivity and better client retention, not just by cutting costs. If you ignore the hidden costs of data cleaning, you risk a failed implementation that yields zero return.

How can mobile-first workflows drive advisor productivity?

Mobile-first CRM capabilities, including social networking and mobile access, can increase sales representative productivity by 26.4%. This allows advisors to perform KYC and portfolio reviews directly from a 360-degree Customer Dashboard on mobile devices.

Advisors can leverage a 360-degree Customer View to centralize financial information, interactions, and history. This allows for informed, real-time decision-making during client meetings.

Mobile-first workflows provide several key advantages:

- Real-time KYC: Advisors can initiate and complete Know Your Customer (KYC) processes on the spot using mobile document scanning and biometric verification.

- Immediate Portfolio Reviews: Using the 360-degree Customer Dashboard, an advisor can pull up a client’s current asset allocation and suggest adjustments during a live meeting.

- Enhanced Client Engagement: Mobile access allows for immediate follow-ups and updates, ensuring the client feels prioritized.

In testing various mobile interfaces, the biggest friction point remains the complexity of data entry. A mobile CRM that requires 15 taps to log a simple meeting will be ignored. The most successful tools prioritize “one-tap” actions and voice-to-text capabilities to ensure the CRM supports the advisor rather than hindering them.

FAQ

What is the difference between Next Best Action and Next Best Client?

Next Best Action focuses on optimizing interactions with existing clients to improve retention and service. In contrast, Next Best Client uses predictive AI to identify future high-value prospects by analyzing life event signals and wealth indicators.

How much can a bank expect to gain from a CRM investment?

Financial organizations can expect significant returns. Reports indicate that for every $1 spent on CRM implementation, companies can achieve a return on investment (ROI) of $8 through improved efficiency and client growth.

Why is ‘explainable AI’ critical for wealth management in 2026?

Regulators are increasing scrutiny on algorithmic decisions. Explainable AI ensures that all automated recommendations, such as those generated by predictive targeting models, have a clear, auditable reasoning trail to prevent compliance failures.

Advertisement