Advertisement

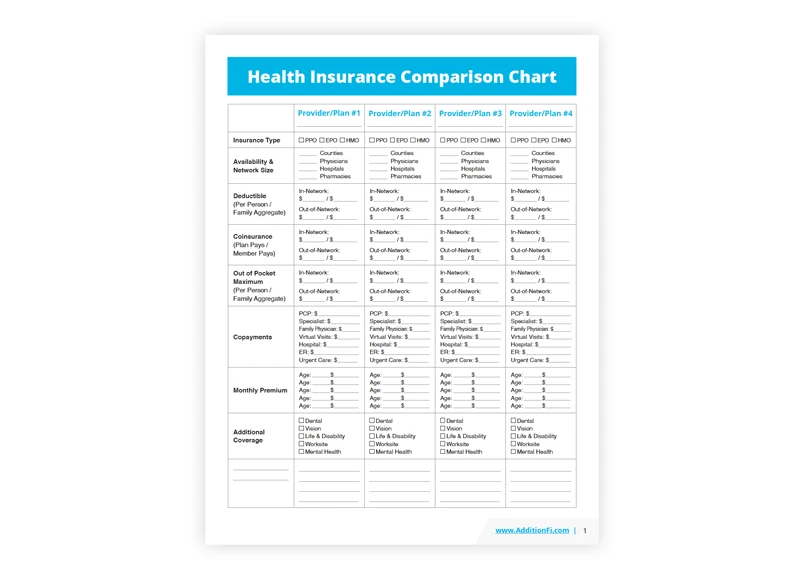

CRM FanzineFaves – To compare insurance policies effectively, you must look beyond the monthly premium. Evaluate the Total Cost of Ownership by weighing deductibles against coverage limits, analyze the distinction between collision and comprehensive protections, and use digital tools to compare current declarations against new quotes to identify hidden coverage gaps.

Collision insurance is typically 122% more expensive than comprehensive insurance, making the choice between them a critical driver of your total auto insurance spend.

How do you decode insurer jargon to compare policies accurately?

To ensure your protection is consistent, use the technique of Reviewing insurance endorsements. Compare endorsement language directly against the contract to identify any conflicts in coverage limits or exclusions that might alter your base policy.

Advertisement

The Terminology Decoder: Translating Jargon

Many consumers fall into the trap of assuming two quotes from companies like GEICO or Allstate are identical because the premium amounts are similar. This is a common failure mode. To avoid this, you must engage in Reviewing Insurance Endorsements. An endorsement is an amendment that can either expand or restrict your base coverage. If you do not compare endorsement language directly against the contract, you may find that a “full coverage” claim is denied because a specific exclusion was added via a rider.

Use these specific categories to build an apples-to-apples comparison:

- Coverage Limits: The maximum amount the insurer will pay for a single incident or over the life of the policy.

- Deductibles: The specific dollar amount you pay before the insurer covers a loss.

- Exclusions: Specific scenarios, such as certain types of weather or driver profiles, that the policy will not cover.

- Endorsements: Custom additions or subtractions to your standard policy terms.

Using AI to Standardize Your Current Policy

Manually reading 50-page policy booklets is inefficient and prone to human error. Modern Insurify tools offer an AI-powered policy upload feature to solve this. By using the Insurify AI Policy Upload, you can simply upload a picture of your current policy declaration page. The system then extracts your existing limits and deductibles, allowing you to compare them side-by-side with new quotes. This prevents the mistake of comparing a $500 deductible policy against a new quote that secretly carries a $1,000 deductible.

What is the ‘Claims Experience Scorecard’ for evaluating insurers?

Evaluate insurers by analyzing the data found in Insurify Insurer Snapshots. These snapshots aggregate over 85,000+ ratings and reviews to provide data on actual payout speed and dispute resolution history.

Moving Beyond Marketing Ratings

A high customer service score does not guarantee a smooth claims process. An insurer might have a friendly call center but a notoriously slow payout cycle. To build a true scorecard, you must look at the Insurer Snapshots provided by platforms like Insurify. These snapshots aggregate data from over 85,000+ ratings and reviews to give you a more granular view of how companies actually behave when a claim is filed. A company might rank highly for “ease of use” but fail significantly on “payout speed.”

Shortcut: To quickly assess an insurer’s reputation, navigate to the Insurify platform and search for the “Insurer Snapshots” section to view aggregated user feedback.

Metrics That Matter: Payout Speed vs. Customer Service

When evaluating efficiency, look for specific mentions of “digital claims filing” in the 85,000+ user reviews available via Insurify. This metric often serves as a more reliable indicator of how quickly a claim is processed than general customer service ratings.

Should you choose Collision or Comprehensive coverage?

Collision insurance is designed for accidents where you hit another vehicle or object. In contrast, comprehensive coverage pays for damages regardless of fault, such as theft or weather events.

Understanding the Cost Gap

The financial difference between these two coverages is substantial. Based on recent data, the average auto collision insurance claim sits at $4,822, whereas the average comprehensive insurance claim is significantly lower at $1,284. Because collision coverage involves higher-risk scenarios like multi-vehicle accidents, the premiums reflect that risk. The following table illustrates the primary differences you will encounter when comparing these two options.

Coverage Type |

Primary Trigger |

Typical Cost Level |

Key Benefit |

|---|---|---|---|

Collision |

Hitting another vehicle or object |

High (122% more) |

Covers at-fault accidents |

Comprehensive |

Theft, fire, or weather events |

Lower |

Covers non-collision damage |

Budgeting for these costs requires accounting for the 122% premium difference between collision and comprehensive options.

When to Prioritize One Over the Other

Your decision should align with your asset’s value. While comprehensive coverage is necessary to protect against theft or falling debris, the higher cost of collision insurance may not be mathematically sound for vehicles with low market value.

What are the hidden pitfalls in auto insurance comparisons?

Common pitfalls include choosing an excessively low premium that only meets minimum state requirements, creating coverage gaps by using personal policies for commercial purposes (like ride-sharing), and failing to account for how higher deductibles increase out-of-pocket costs during a claim.

Warning: Using a personal auto policy for commercial purposes, such as delivering pizzas or operating a delivery service, will result in a total denial of coverage during a claim.

The Commercial Use Trap

A major risk factor in insurance comparisons is the “Coverage Gap.” Many drivers assume that because they have a standard policy, they are protected while working for apps like Uber or DoorDash. This is false. Personal auto insurance will not provide coverage if you use your car for commercial purposes. If you fail to disclose this usage, the insurer will likely deny the claim entirely, leaving you with 100% of the repair costs.

The Deductible vs. Premium Trade-off

It is a common misconception that a lower monthly premium always equals a better deal. In many cases, a low premium is achieved by setting an extremely high deductible. While this lowers your monthly bill, it adds massive payout-of-pocket costs when a claim occurs. For example, a policy might save you $20 per month, but if you have a $1,000 deductible, you must endure 41 months of “savings” just to break even on a single claim event. This creates significant financial vulnerability if you do not have emergency savings available.

How can digital marketplaces speed up your comparison?

Digital marketplaces like Insurify allow you to compare quotes from over 120 insurers simultaneously. By using features like AI-powered policy uploads, you can compare your current coverage side-by-side with new options to ensure you aren’t sacrificing protection for a lower price.

Comparing InsureTech vs. Traditional Brokers

Traditional brokers often rely on manual data entry, which can lead to inaccurate quotes if your driving history or health details are not entered perfectly. Digital marketplaces utilize automated data fetching to minimize these errors. Furthermore, while a broker might only present 3 or 4 options, a marketplace provides access to over 120+ insurers, significantly increasing your chances of finding a competitive rate. In some cases, users have reported potential savings of up to $1,100 by utilizing these digital platforms.

Maximizing Savings with Marketplace Tools

Follow these steps to optimize your search:

- Use the AI Upload: Avoid manual entry errors by uploading your current declaration page.

- Check the Review Aggregates: Don’t just look at the price; look at the insurer’s reputation in the “Insurer Snapshots” section.

- Verify the Coverage Details: Ensure the new quote includes the same endorsements you currently hold.

- Compare Total Cost: Calculate the total annual cost (Premium x 12 + Deductible) rather than just the monthly rate.

FAQ

Will my personal auto policy cover me if I drive for Uber or DoorDash?

No. Personal auto policies will not provide coverage if you use your car for commercial purposes, such as delivering pizzas or operating a delivery service.

How does a higher deductible affect my premium?

Choosing a higher deductible lowers your premium but increases your out-of-pocket costs during a claim event.

Is collision insurance more expensive than comprehensive?

Yes, collision insurance is usually more expensive, often costing 122% more than comprehensive coverage.

Advertisement