Advertisement

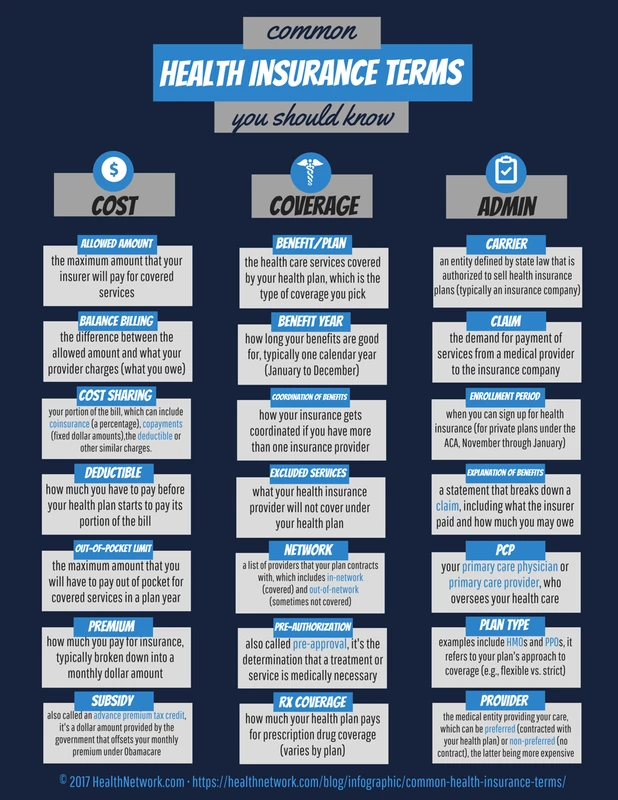

CRM FanzineFaves – Health insurance terms define how costs are shared between you and your insurer. Key concepts include premiums (monthly fees), deductibles (the amount you pay before insurance kicks in), copayments (fixed fees per visit), and coinsurance (your percentage of a claim). Understanding these terms is essential to managing medical expenses and avoiding surprise bills.

The average copayment for a hospital admission is approximately $343, according to KFF statistics.

How does a medical bill actually get processed?

A medical bill flows through three stages: first, you pay your deductible until it is met. Second, you enter the coinsurance phase where you and the insurer split costs (e.g., 80/20). Finally, once you reach your out-of-pocket maximum, the insurer pays 100% of covered services.

Advertisement

The Deductible Phase

Before your insurance company begins sharing costs, you must satisfy your annual deductible. For example, if your plan has a $1,000 deductible, you are responsible for the first $1,000 of covered medical expenses within a 12-month period. Many people mistakenly believe insurance starts paying immediately, but this is a common failure mode that leads to unexpected debt. You can often track your progress toward this amount by logging into your insurer’s member portal and navigating to > Account Summary > Benefits & Coverage.

The Coinsurance Phase

Once the deductible is satisfied, you enter the coinsurance stage. In this phase, the cost-sharing shifts to a percentage-based model. A common arrangement is 80/20, where the insurance company pays 80% of the allowed amount and you pay the remaining 20%. This continues until you hit a specific financial ceiling. It is counterintuitive, but even after you meet your deductible, you are still responsible for a portion of every bill.

Reaching the Out-of-Pocket Limit

The out-of-pocket maximum serves as your financial safety net. Once your total spending—including deductibles, copayments, and coinsurance—reaches this threshold, the insurer pays 100% of covered costs for the remainder of the plan year.

- Deductible: The initial amount paid out-of-pocket before insurance coverage begins.

- Coinsurance: The percentage of costs (e.g., 20%) shared between the patient and the insurer.

- Out-of-pocket Maximum: The maximum amount you pay before the insurer covers 100% of costs.

How do you read an Explanation of Benefits (EOB)?

An Explanation of Benefits (EOB) is not a bill; it is a document showing how your insurer processed a claim. It details the ‘Allowed Amount’ (the negotiated rate), what the insurer paid, and your ‘Patient Responsibility’ (the amount you actually owe the provider).

“Health insurance in the U.S. is complicated and very different from the medical practices of other countries,” notes the Harvard International Community. This complexity is most visible when reviewing an EOB, which can be overwhelming for new policyholders.

Allowed Amount vs. Billed Amount

A major point of confusion is the difference between what a doctor charges and what the insurance company actually covers. As stated by WPS, “Allowable charge—sometimes known as the ‘allowed amount,’ ‘maximum allowable,’ and ‘usual, customary, and reasonable (UCR)’ charge, this is the dollar amount considered by a health insurance company to be a reasonable charge for medical services or supplies based on the rates in your area.” If a provider bills $500 for an office visit but the allowed amount is only $100, you should not be held responsible for the $400 difference if the provider is in-network.

Identifying Your Responsibility

To avoid overpaying, you must verify the “Patient Responsibility” section of the document. This figure represents the sum of your copayments and coinsurance. A frequent failure occurs when patients pay the “Billed Amount” sent by a doctor’s office instead of waiting to reconcile it with the EOB. Always cross-reference your provider’s invoice with the EOB before sending payment.

Shortcut: To view your recent claims digitally, log into your insurer’s website and go to > Claims > View/Print EOB.

What is the difference between HMO and PPO plans?

HMO plans typically charge lower premiums than other health insurance options. These plans require a primary care physician to act as a gatekeeper for all referrals and specialist access.

Deciding between these models involves weighing cost against access. While HMOs offer lower monthly costs, PPOs provide more freedom to see providers without a referral.

Feature |

HMO (Health Maintenance Organization) |

PPO (Preferred Provider Organization) |

|---|---|---|

Cost (Premiums) |

Typically lower monthly costs |

Typically higher monthly costs |

Flexibility |

Limited; requires referrals |

High; no referrals needed |

Network Requirements |

Must use in-network providers |

Can use out-of-network (at higher cost) |

Gatekeeper Model |

Requires Primary Care Physician (PCP) |

No PCP required |

The table above illustrates the fundamental trade-off between cost and access. As Equifax notes, “In exchange for this increased flexibility, a PPO is typically more expensive than an HMO.”

The Gatekeeper Model in HMOs

In an HMO, your Primary Care Physician (PCP) acts as a coordinator for all your healthcare needs. This is known as the Gatekeeper Model. If you need to see a dermatologist or a cardiologist, you must first visit your PCP to obtain a formal referral. This system is designed to control costs and ensure that specialist visits are medically necessary.

Network Flexibility in PPOs

PPO networks tend to be larger and more flexible than HMO counterparts. This allows you to bypass the referral process entirely. If you have a specific specialist you wish to see, a PPO gives you the freedom to book an appointment directly. However, you will generally pay less for services received from in-network providers because they have negotiated discounts with the insurer.

What are the most common copayment costs?

Copayments are fixed fees paid at the time of service. Common examples include $26 for a primary care visit, $42 for a specialist, $250 for emergency care, and $10 for generic medications, though these vary by plan.

These flat dollar amounts are usually collected at the front desk of a clinic or pharmacy. For example, a generic drug copay might be as low as $10.

Primary Care vs. Specialist Fees

Insurance plans use different copayment amounts to manage provider utilization. Typical costs include:

- $26 for a primary care visit.

- $42 for a visit to a specialist.

- $20 for a standard primary care physician visit (depending on plan).

Emergency and Hospital Copays

Higher-acuity services carry significantly higher copayments to discourage the unnecessary use of emergency departments for minor ailments. For instance, an emergency medical care copay can reach $250. Hospital admissions can be even more costly, with the average copayment for a hospital admission sitting at approximately $343. Additionally, pharmacy copayments are often tiered, with generic drugs costing as little as $10 per prescription.

Why might an insurance claim be denied?

Claims are most commonly denied due to policy exclusions (services not covered), lack of pre-authorization, or services deemed not medically necessary. Out-of-network usage in restricted plans is another frequent cause of unexpected costs.

If a claim is denied, you should immediately review the reason provided by your insurer. You may need to file an appeal to resolve the discrepancy.

Exclusions and Medical Necessity

Insurers use exclusions to narrow responsibility and reduce payouts, especially after serious accidents. An exclusion is a specific service or condition that your policy explicitly states will not be covered. Furthermore, a claim might be denied if the insurer decides the treatment was not “medically necessary.” This is a subjective determination that can often be challenged by your doctor through an appeal.

The Importance of Pre-Authorization

One of the most common pitfalls is failing to obtain pre-authorization. This is a process where the health plan must approve coverage for a service requested by a doctor or patient before receiving it. If you undergo an expensive procedure, such as an MRI or surgery, without this prior approval, the insurer may deny the claim entirely. To prevent this, always ask your provider’s billing department: “Has this service been pre-authorized by my insurance?”

FAQ

What is the difference between Medicaid and Medicare?

Medicare is a federally funded health insurance program designed for individuals aged 65 or older or those with specific disabilities. In contrast, Medicaid is a state-sponsored assistance program intended for low-income individuals, such as Medi-Cal in California.

Is a pre-existing condition exclusion still legal?

No, pre-existing condition exclusion is illegal in most cases due to federal protections. This ensures that individuals with chronic or past illnesses cannot be denied coverage or charged higher rates based on their medical history.

What does ‘Coordination of Benefits’ mean?

Coordination of Benefits is a system used in group health plans to prevent the duplication of benefits. It determines which insurance plan pays first when a person is covered by more than one policy, ensuring the total payment does not exceed 100% of the allowed amount.

Advertisement