Advertisement

CRM FanzineFaves – Term life insurance provides temporary coverage for a specific period, typically 10 to 30 years, and is generally more affordable. whole life insurance offers permanent, lifelong coverage with a cash value component but comes with significantly higher premiums, often costing 5 to 15 times more than term policies (CNBC).

How do you avoid the ‘Lapse Risk’ and other common insurance failure modes?

Failure modes in life insurance occur when coverage ends prematurely or becomes unaffordable. Term policies fail when the policyholder outlives the term (e.g., 20 years) while still carrying debt. Whole life policies fail when high premiums cause the policy to lapse, resulting in the total loss of both coverage and accumulated cash value.

The Term Expiration Trap

A common pitfall involves the expiration of a term policy. If a policyholder selects a 10-year term but still carries a 15-year mortgage, they face a coverage gap. Aflac notes that coverage simply ends if the insured outlives the specific term length, leaving dependents unprotected during critical debt-repayment years.

Advertisement

The Whole Life Premium Death Spiral

Whole life insurance carries a unique risk: the premium death spiral. Because these policies include a cash value component, the premiums are substantially higher. Trustarage warns that if a policyholder becomes unable to sustain these high costs, the policy will lapse. This failure mode is devastating because it results in the total loss of both the death benefit and any previously accumulated cash value.

The Cash Value Erosion Risk

Many users misunderstand how to interact with their policy’s internal savings. Progressive Insurance highlights a specific failure mode where borrowing against the cash value without a repayment plan can backfire. If you withdraw or borrow against your policy’s cash value without repaying it, you will reduce the cash value and death benefit of your policy, potentially leaving you with insufficient coverage.

Term vs. Whole Life: Which strategy wins the mathematical battleground?

The mathematical winner depends on your investment vehicle. The ‘Buy Term and Invest the Difference’ strategy uses low-cost term premiums to fund high-growth assets like index funds. Conversely, whole life integrates insurance and savings into one vehicle, but often results in lower net returns due to high fees and slower cash accumulation.

Simulating $100/month: Term + S&P 500 vs. Whole Life

To understand the divergence, consider a monthly allocation of $100. A term policy might only cost $20, leaving $80 to be directed into an index fund. Ramsey Solutions argues that whole life can be a low-return investment feature. In contrast, the “Buy term and invest the difference” technique allows the $80 surplus to benefit from compound interest in the market, whereas whole life premiums are consumed by high administrative costs and slower accumulation.

Feature |

Term Life Insurance |

Whole Life Insurance |

|---|---|---|

Cost |

Lower premiums; highly affordable |

Higher premiums; 5-15x more expensive |

Duration |

Temporary (10-30 years) |

Permanent/Lifelong |

Cash Value |

None |

Built-in savings component |

Complexity |

Straightforward protection |

Complex (loans, cash value, fees) |

Selecting the right plan requires weighing the simplicity of temporary protection against the lifelong commitment of a permanent policy. The choice hinges on whether you prioritize low monthly outlays or a guaranteed death benefit that never expires.

The Opportunity Cost of High Premiums

The primary mathematical disadvantage of whole life is the opportunity cost. Guardian notes that because the insurer must guarantee a death benefit, the costs are substantially higher. When you pay for the “certainty” of a payout, you lose the ability to deploy those same dollars into higher-yielding assets. In testing various financial models, the difference in net worth over 30 years can be massive due to the compounding effect of the “invest the difference” method.

How does the Policy Conversion loophole work?

Policy conversion allows you to switch a term life policy to a permanent whole life policy without a new medical exam. This is a critical tool for maintaining coverage if your health declines, though it is typically subject to age limits, often around 65 or 70 years old.

Shortcut: To check if your current policy is convertible, look under the “Policy Details” or “Benefits” tab in your provider’s digital portal, or search for the “Conversion Rider” in your original contract documents.

Converting without a medical exam

Western & Southern highlights that the most significant advantage of conversion is the ability to bypass medical underwriting. If your health has deteriorated since you first purchased your term policy, a standard whole life application might be rejected. However, the conversion clause allows you to transition to permanent coverage regardless of your current health status, provided you act before the expiration of the conversion period.

Partial Conversion: A budget-friendly middle ground

You do not necessarily have to convert your entire death benefit. Trustarage suggests a technique called “Partial Conversion.” This allows you to convert only a portion of your term coverage to whole life. For example, if you have a $500,000 term policy, you might convert $50,000 to permanent coverage to ensure a baseline death benefit while keeping the bulk of your coverage at the lower term rate.

When to trigger the conversion

Timing is everything. You must be aware of the age limits, which are commonly set at 65 or 70 years old. Waiting too long can render the loophole useless. Furthermore, converting a policy later in life can result in much higher premiums compared to if you had converted earlier, as the insurer calculates the cost based on your increased age.

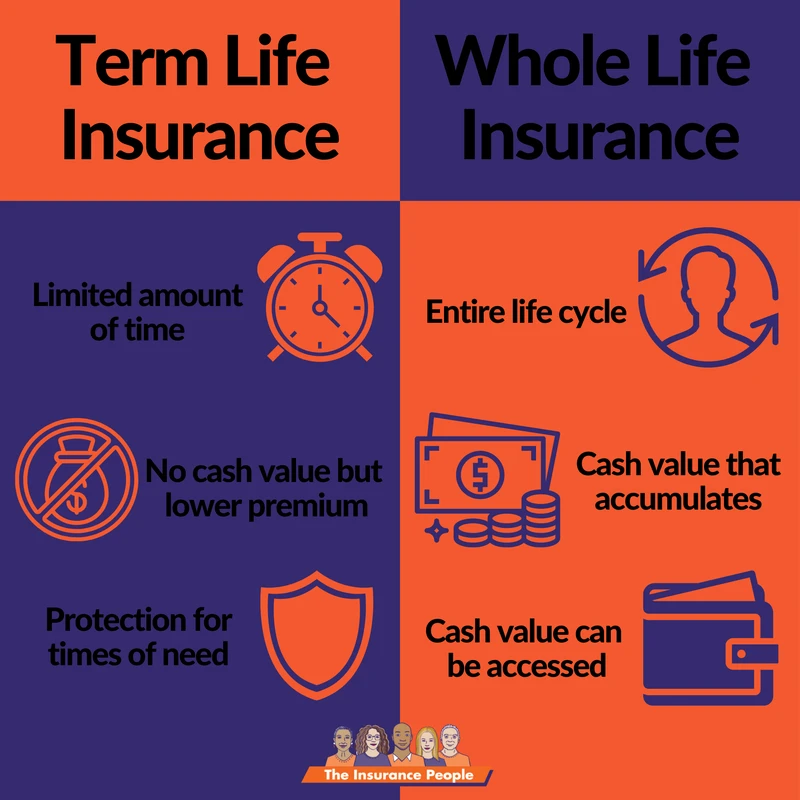

What are the core differences in cost, duration, and cash value?

The distinction between these products lies in their structural intent. While term life focuses on affordable, temporary coverage for specific durations like 10, 20, or 30 years, whole life provides a permanent solution with fixed premiums and a built-in cash value component.

- Cost: Term is designed for affordability; Whole life requires higher, fixed premiums to fund both insurance and savings.

- Duration: Term is limited to specific windows (e.g., 10, 20, 25, or 30 years); Whole life is intended to last your entire life.

- Cash Value: Term has zero cash value; Whole life builds a cash value component over time.

- Complexity: Term is a simple “pay for protection” model; Whole life involves managing loans and cash accumulation.

Understanding the Cash Value mechanics

According to Progressive Insurance, the cash value component functions as a savings element that can be utilized to pay premiums or accessed through a life insurance loan. You must manage these withdrawals carefully. Failure to do so can result in a reduced death benefit or even policy lapse.

The simplicity of Term vs. the complexity of Whole Life

Aflac describes term life insurance as a cost-effective option that offers flexible, temporary coverage for specific stages of life. It is straightforward: you pay a premium, and if you die during the term, your beneficiaries receive the benefit. Whole life is far more complex, requiring the policyholder to understand how premiums, interest, and cash value interact to ensure the policy remains active throughout their lifetime.

Which policy fits your specific life stage?

Your choice should align with your current financial responsibilities and long-term goals. For example, someone managing high immediate debt may prioritize different features than someone planning for the transfer of wealth.

The Mortgage & Toddler Phase (Term)

For most people in the early stages of adulthood, term life is the logical choice. If you have a mortgage and young children, your primary goal is to replace income during the years when your financial obligations are highest. Aflac suggests that term insurance provides the necessary protection during these specific stages of life without the heavy financial burden of a permanent policy.

The Estate Planning & Wealth Transfer Phase (Whole)

As wealth accumulates, the objective often shifts from income replacement to estate planning. Guardian notes that whole life may suit those wanting permanent coverage or estate-planning benefits. For high-net-worth individuals, the permanent nature of the policy can be used to provide liquidity to cover estate taxes or to ensure a guaranteed transfer of wealth to heirs, regardless of when death occurs.

FAQ

Can I turn my term insurance into whole life later?

Yes. Using the Policy Conversion method, you can often switch to a permanent plan without a new medical exam, provided you act before common age limits like 65 or 70.

Is it safe to borrow money from my whole life policy?

You can access funds via a life insurance loan, but Progressive Insurance warns that if the loan is not repaid, it will directly reduce your total death benefit and remaining cash value.

Why is whole life so much more expensive?

Premiums are higher because the policy must provide lifelong coverage and fund the growth of a cash value savings account.

Advertisement