Advertisement

CRM FanzineFaves – Choosing between single-trip and annual travel insurance depends on your travel frequency and trip length. Single-trip insurance is best for infrequent travelers or long journeys exceeding 90 days. Annual insurance offers better value if you take three or more trips per year, providing convenience for spontaneous travel within a 12-month period.

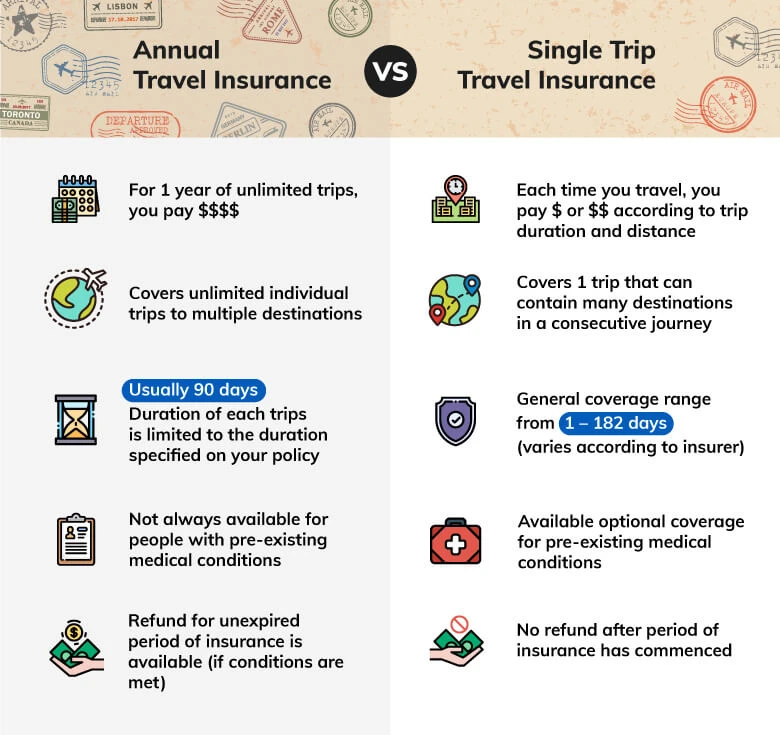

According to The AA, annual travel insurance can offer better value if you plan to take three or more trips in a year.

Is Annual Insurance Actually Cheaper? The Mathematical Stress Test

Annual insurance becomes cost-effective when you exceed the ‘break-even’ threshold, typically 3 to 4 trips per year. However, a single major claim can deplete your ‘aggregate benefit pool,’ potentially leaving you unprotected for subsequent trips in that same year.

Advertisement

While the upfront premium for an annual policy might seem lower than buying three individual plans, the math changes once you factor in benefit exhaustion. If you are using an online portal to compare plans, navigate to Settings > Policy Details > Coverage Limits to see how your benefits are structured. A common misconception is that annual insurance provides “unlimited” protection for the year; in reality, most providers like Travel Guard or Allianz Partners utilize an aggregate limit that applies to the entire 364-day period.

The ‘Bucket Metaphor’: Understanding Aggregate Limits

Think of your annual coverage as a single bucket of water representing your total available benefits. Every time you file a claim—whether it is a $500 lost bag or a $10,000 medical emergency—you are scooping water out of that bucket. If you have a massive claim on your first trip in January, your bucket might be nearly empty by the time you attempt your third trip in October. This is a critical failure mode that single-trip policies avoid, as their coverage limits reset to 100% for every new journey you insure.

Worst-Case Scenario: One Claim vs. Three Trips

If a traveler on an annual plan suffers a significant medical event on Trip 1, the aggregate limit for the 364-day period may be exhausted. This leaves the traveler without coverage for the remainder of the year. Conversely, a traveler using three separate single-trip plans benefits from coverage limits that reset for every new journey. The following table demonstrates the financial and coverage implications of these two approaches.

Scenario Metric |

Annual Multi-Trip Plan |

Three Single-Trip Plans |

|---|---|---|

Initial Cost Structure |

One upfront premium |

Three separate premiums |

Benefit Reset |

No; benefits decrease per claim |

Yes; limits reset every trip |

Claim Exhaustion Risk |

High (Aggregate limit applies) |

Low (Each trip is isolated) |

Spontaneity Factor |

High; ready for any trip |

Low; must buy before every departure |

The data confirms that while annual plans offer convenience, they carry a risk of benefit depletion. You must weigh the ease of spontaneous travel against the security of reset limits.

Do You Already Have Coverage? The Credit Card vs. Annual Policy Matrix

Many premium credit cards offer built-in travel insurance, which can lead to ‘double coverage’ or redundant spending. Before buying an annual policy, audit your card benefits to see if they cover your specific needs like trip cancellation or medical emergencies.

It is a common mistake to assume that having a high-tier credit card makes additional insurance unnecessary. While cards from major issuers often provide some level of protection, they frequently operate on a secondary basis. This means you might find yourself in a billing loop where you must first exhaust your personal health insurance before the card benefits kick in. To check your specific coverage, log in to your banking app and go to Settings > Policy Details > Coverage Limits to see how your benefits are structured. To check your specific coverage, log in to your banking app and go to Benefits > Cardholder Protections > Travel Insurance.

Shortcut: Before purchasing a new policy, call the number on the back of your premium credit card and ask specifically: “Is my travel medical coverage primary or secondary?”

Redundancy Audit: Checking your Card’s Fine Print

A redundancy audit prevents you from paying for the same protection twice. For example, if your credit card already provides $50,000 in trip interruption coverage, buying an annual policy with the same benefit is a waste of capital. However, many card benefits are limited to specific types of travel, such as trips fully paid for with that specific card. If you use a different method for your flight booking, the card’s coverage may fail entirely.

Primary vs. Secondary Medical: The Billing Order Trap

The distinction between primary and secondary coverage is where most travelers encounter friction. According to Allianz Partners, single-trip plans often offer primary emergency medical benefits. This is a massive advantage because the travel insurer pays the hospital directly without involving your domestic health provider. Multi-trip plans, however, frequently offer secondary benefits. In this scenario, your personal health insurance is billed first, and you are left responsible for any co-pays or deductibles that the primary insurer refuses to cover.

How Do Trip Durations Differ Between the Two Plans?

Single-trip plans are superior for long-term travel, often covering durations from 94 to 365 days. In contrast, annual policies usually impose a strict ‘per-trip’ limit, typically capping individual journeys at 30 to 90 days.

If you stay in one location for longer than the stated per-trip limit, your policy may become invalid. Many annual policies are designed for frequent vacationers rather than long-term stays. You must be aware of these specific constraints:

- Annual Per-Trip Limits: Commonly capped at 30 to 45 days or 30 to 90 days depending on the provider.

- Single-Trip Flexibility: Can be tailored for durations ranging from 94 to 180 days or even up to 365 days for long-term stays.

- Consecutive Travel Rules: Annual plans may require you to return to your home country to “reset” the trip duration.

The Nomad’s Dilemma: Avoiding the Per-Trip Limit

The Nomad’s Dilemma occurs when a traveler buys an annual policy for convenience but fails to realize their 60-day stay in Thailand exceeds the 30-day per-trip limit found in many standard annual contracts. This is a major failure mode. If you find yourself staying longer than expected, you must check your policy via the provider’s mobile app or website under Policy > Trip Duration Rules to avoid a total loss of coverage.

Single-Trip Flexibility for Extended Stays

For travelers embarking on a single, extended journey, single-trip insurance is the only logical choice. These plans allow you to define a specific start and end date, providing coverage for the entire duration, whether it is 120 days or a full year. This specificity ensures that you are not fighting against arbitrary “per-trip” caps that exist in multi-trip frameworks.

What Are the Most Common Reasons for Claim Rejection?

Claims are most frequently denied due to non-disclosure of pre-existing medical conditions, traveling to destinations with official government ‘Do Not Travel’ warnings, or seeking coverage for routine/preventative medical care rather than sudden emergencies.

To avoid claim denial, verify that your travel does not violate specific policy terms. For instance, if you are traveling to a country where the Department of Foreign Affairs (DFA) has issued a “Do Not Travel” warning, your insurance company will likely refuse to honor any claims arising from that trip.

The Non-Disclosure Trap: Medical History Matters

Failing to declare pre-existing medical conditions is a leading cause of claim rejection. If you have a history of asthma and suffer a respiratory emergency abroad, the insurer will investigate your medical records. If they find a prior diagnosis that was not disclosed during the application process, they can deny the claim entirely. This is not a matter of interpretation; it is a contractual breach. To prevent this, ensure you review your medical history against the insurer’s specific disclosure requirements before clicking “purchase.”

When Government Warnings Invalidate Your Policy

Insurance is a contract based on “foreseeable risk.” If a government body like the DFA issues a high-level warning regarding civil unrest or health crises in a specific region, the risk becomes “foreseeable.” Traveling to these areas effectively voids your coverage for incidents related to those warnings. Furthermore, claims arising from substance use—such as excessive alcohol consumption—are almost universally rejected by providers like Seven Corners and JustCover.

Which Plan Should You Choose? A Quick Decision Guide

Your decision depends on your itinerary. If you are planning a single journey of 94 to 365 days, single-trip insurance is the standard. For those planning 3 or more trips within a 12-month period, an annual policy may provide better value.

To make the final determination, you should perform a “Spontaneity vs. Security Audit.” This involves looking at your calendar for the next 12 months and your specific medical needs. As Letitia Smith, a Travel Insurance Expert, states: “If you’re only going away once or twice, a Single Trip policy may be more cost-effective. If you’re a regular traveller, love last-minute breaks, or plan multiple holidays throughout the year, an Annual Multi-trip policy can offer better value and peace of mind.”

Feature |

Single-Trip Insurance |

Annual Multi-Trip Insurance |

|---|---|---|

Travel Frequency |

1–2 times per year |

3+ times per year |

Trip Duration Limits |

Flexible (up to 365 days) |

Strict (typically 30–90 days per trip) |

Medical Benefit Type |

Often Primary |

Often Secondary |

Cost Predictability |

Varies per trip |

Fixed annual premium |

Compare your travel profile to the features in the table above to select the appropriate policy type.

Persona-Based Recommendations

If you fall into the “Once-a-Year Vacationer” category, stick to single-trip plans. You get higher coverage limits, primary medical benefits, and no risk of aggregate benefit depletion. If you are a “Weekend Warrior” or “Frequent Flyer” who takes short trips every few months, the annual plan’s convenience and cost-savings will outweigh the secondary medical risks.

The Spontaneity vs. Security Audit

Ask yourself these three questions to finalize your choice:

- Will any of my planned trips exceed 30 days in a single location?

- Do I have a pre-existing condition that requires strict, primary medical coverage?

- Am I planning to travel more than three times in the next 12 months?

FAQ

Can I use annual insurance for a trip longer than 90 days?

Generally no; most annual plans have a per-trip limit of 30 to 90 days. For longer stays, a single-trip policy is required to ensure you are not traveling without valid coverage.

Does annual insurance cover pre-existing medical conditions?

It depends on disclosure. Failing to declare conditions is a top reason for rejection. Always check if the annual policy requires specific underwriting or if you need to add a medical rider.

What is the difference between primary and secondary medical coverage?

Primary coverage pays first without involving your health insurance; secondary coverage requires you to bill your personal health insurance first, which can delay your claim processing.

Advertisement