Advertisement

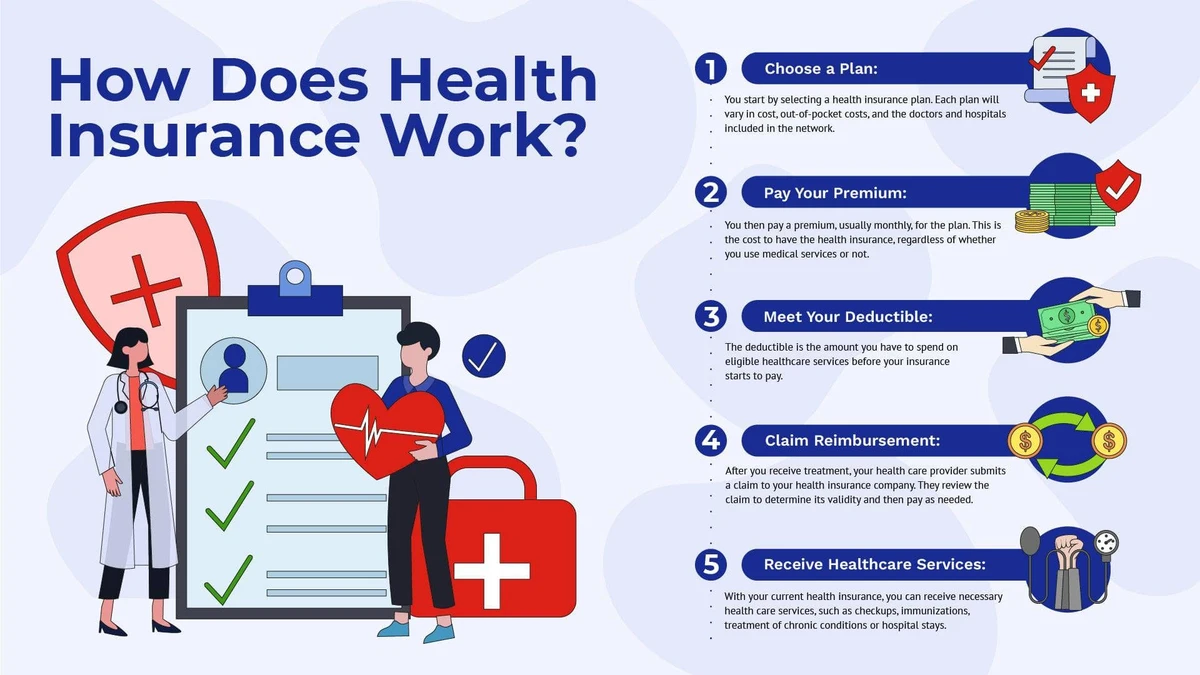

CRM FanzineFaves – Health insurance is a legal contract that shares the financial burden of medical costs between you and an insurer. It covers expenses ranging from routine doctor visits to emergency hospitalizations, typically involving a monthly premium, a deductible you pay first, and coinsurance where costs are split between you and the provider. The Affordable Care Act (ACA), enacted in 2010, expanded coverage to an estimated 20 million people.

How do I calculate the true cost of a health plan?

To find the true cost, do not look at premiums alone. Use the total annual cost formula: (Annual Premiums) + (Expected Copays/Visits) + (Expected Coinsurance) + (Expected Deductible). This accounts for both fixed monthly costs and variable usage-based expenses.

Focusing only on premiums ignores the full cost of care. Many consumers fall into the trap of selecting the lowest monthly payment, only to face a $7,500 bill during a hospital emergency because their deductible was too high. This failure mode can lead to severe financial insecurity when unexpected medical needs arise.

Advertisement

In testing various plan structures, I found that a plan with a $300 deductible and higher monthly premiums often costs less annually for a person with chronic needs than a “cheap” plan with a $5,000 deductible. You must use a Cost Comparison Strategy to see the full picture.

Shortcut: To perform a quick audit, navigate to your insurer’s member portal > Benefits & Coverage > Summary of Benefits and Coverage (SBC) to find the exact breakdown of your out-of-pocket limits.

The Premium vs. Out-of-Pocket Trade-off

A low monthly premium may not be the best match for you. If you require frequent healthcare, a plan with a slightly higher premium but a lower deductible may save you significant money over a 12-month period.

The ‘Plan Selection Math’ Toolkit

When comparing Plan A and Plan B, use the following logic. If Plan A has a $500 monthly premium and a $10 copay per visit, while Plan B has a $400 premium and a $40 copay, calculate your “break-even” point. If you visit the doctor more than 10 times a year, Plan A is actually the cheaper option.

Why might a ‘covered’ drug or procedure still cost you hundreds?

Costs vary due to pharmacy formularies and prior authorization. Even if a drug is “covered,” it may fall into a high-cost tier, or your insurer may require prior authorization—an administrative hurdle that must be cleared before the service is paid for.

Drug coverage varies significantly between plans with similar premiums. Two different insurance providers might offer nearly identical monthly rates, but one might place your specific medication in a high-cost tier while the other places it in a low-cost tier. This discrepancy can result in a difference of hundreds of dollars at the pharmacy counter.

Decoding Pharmacy Tiers

Insurance companies use a Drug Coverage Review process to categorize medications. Most plans use a tier system: Tier 1 usually covers low-cost generics, while Tier 4 might cover specialty drugs that require significant out-of-pocket spending. Always check your plan’s formulary before starting a new prescription.

The Prior Authorization Trap

A common failure mode occurs when a doctor prescribes a treatment that requires prior authorization. If your provider fails to submit the necessary clinical documentation to the insurer before the procedure, the claim may be denied entirely. This administrative hurdle is a frequent cause of unexpected medical debt.

What are the core components of health insurance terminology?

Key terms include: Premium (monthly fee), Deductible (amount paid before insurance kicks in), Copay (fixed fee per visit), Coinsurance (percentage of cost shared, e.g., 20-40%), and Out-of-Pocket Maximum (the limit on your total yearly spending).

The deductible is the amount you pay out of pocket before your health insurance starts to cover costs. For example, if you have a $300 deductible, you are responsible for the first $300 of covered services. Only after this threshold is met does the insurance company begin sharing the costs through coinsurance.

Term |

Definition |

Typical Value |

|---|---|---|

Premium |

Monthly cost to keep plan active |

Varies by plan |

Deductible |

Amount paid before insurance coverage begins |

Variable (e.g., $300+) |

Copay |

Fixed fee for a specific service |

e.g., $10 |

Coinsurance |

Percentage of cost shared after deductible |

20-40% (Member) / 60-80% (Insurer) |

Out-of-Pocket Max |

The absolute limit on your yearly spending |

Varies |

Once you reach your out-of-pocket maximum, the insurance company typically pays 100% of the costs for covered services for the remainder of the plan year. This is the most critical safety net in your contract, preventing a single catastrophic illness from causing total financial ruin.

The Three Phases of Payment: Deductible, Coinsurance, and Out-of-Pocket Max

Payment follows a specific sequence. First, you pay 100% of costs until you hit your deductible. Second, you enter the coinsurance phase, where you might pay 30% of a bill while the insurer pays 70%. Finally, once your total spending hits the out-of-pocket maximum, the insurer covers 100% of the remaining covered costs.

Which plan type (HMO, PPO, or EPO) is right for you?

Choose an HMO for lower costs and managed care if you don’t mind needing referrals. Select a PPO for the widest network and out-of-network access. Choose an EPO if you want in-network coverage without the strict referral requirements of an HMO.

In Michigan, HMOs are among the most widely offered plan types, and for many small and mid-size employers, they represent the most cost-effective group health option available. However, the trade-off for this cost-effectiveness is limited provider choice.

Plan Type |

Network Access |

Referral Required? |

Typical Cost Level |

|---|---|---|---|

HMO |

In-Network Only |

Yes |

Lower ($450-$600) |

PPO |

In & Out-of-Network |

No |

Higher ($500-$700) |

EPO |

In-Network Only |

No |

Moderate ($470-$640) |

Note that these premium ranges are illustrative for Michigan small group plans per employee per month. When choosing, you must perform a Network Verification to ensure your current preferred doctors and clinics are actually connected to the new plan’s network.

Comparing Network Flexibility and Costs

PPOs offer the broadest provider access, including out-of-network coverage; HMOs are limited to in-network providers. If you travel frequently or want to see specialists without a primary care doctor’s permission, the higher premium of a PPO is often worth the flexibility.

What mistakes should you avoid during enrollment?

Avoid rushing enrollment based on social recommendations, concealing medical history (which leads to denied claims), and ignoring the total cost of care. Also, ensure you do not rely on insurance to replace lost income during illness.

Many people rush into buying their health insurance or rely solely on recommendations from friends, family, and coworkers. To avoid these pitfalls, perform a thorough Policy Document Audit to understand exactly what is excluded from your coverage.

- Do not conceal medical history: This can result in denied claims for existing conditions.

- Do not mistake coverage for income: Health insurance pays for your care, but it doesn’t replace your income if you are unable to work.

- Avoid “Premium-Only” thinking: A low premium might hide a massive deductible that breaks your budget during an emergency.

- Verify your doctors: Never assume your current physician is in-network without checking the insurer’s official directory.

Concealing medical history is a specific pitfall that can ruin your coverage. If an insurer discovers undisclosed medical information, they may deny your claims, leaving you responsible for the entire bill. This is a critical error that can lead to permanent financial instability.

FAQ

How much should my deductible be?

A recommended rule of thumb is to keep your deductible to no more than 5% of your gross annual income to ensure financial stability. If your deductible exceeds this amount, a single medical event could cause significant financial hardship.

What happens after I hit my out-of-pocket maximum?

Once you reach your out-of-pocket maximum, the insurance company typically pays 100% of the costs for covered services for the remainder of the plan year. This provides a ceiling on your total medical expenses.

Can I use out-of-network doctors with an HMO?

Generally, no. HMOs are limited to in-network providers, and using out-of-network services will likely result in no coverage and higher bills. You must stay within the designated network to ensure your costs are shared.

Advertisement