Advertisement

CRM FanzineFaves – Health insurance coverage is determined by your plan’s specific benefits, network restrictions, and cost-sharing structures like deductibles and copayments. To ensure adequate coverage, you must evaluate the total annual cost—combining premiums with out-of-pocket maximums—and verify that your preferred providers are in-network to avoid unexpected balance billing.

As HealthcareInsider.com notes, “A low monthly premium rarely tells the full story.” These lower rates often come with higher deductibles or more restricted coverage options.

How do you calculate the ‘Total Cost of Ownership’ for a health plan?

To calculate the true cost of a health plan, use the ‘Worst Case Scenario’ formula: (Annual Premium × 12) + out-of-pocket maximum. This represents the absolute maximum you would pay in a year of heavy medical usage, providing a more accurate financial baseline than looking at monthly premiums alone.

Advertisement

The ‘Expected Scenario’ vs. ‘Worst Case’ Framework

UnitedHealthcare advises that you must look beyond monthly premiums to factor in deductibles, copays, and out-of-pocket maximums. Budgeting only for the premium leaves you vulnerable to the full cost of a single hospital stay.

In my experience analyzing plan structures, the “Expected Scenario” assumes you only visit a doctor for routine checkups. The “Worst Case Scenario” is the actual mathematical ceiling of your liability. To find this, navigate to your insurer’s digital portal, typically found via a login at myuhc.com or similar provider sites, and locate the “Plan Summary” or “Evidence of Coverage” document.

Cost Component |

Calculation Method |

Financial Impact |

|---|---|---|

Annual Premium |

Monthly Premium × 12 |

Fixed, predictable cost |

Deductible |

Amount paid before coverage |

Variable, based on usage |

Out-of-Pocket Max |

The absolute spending ceiling |

The “Worst Case” limit |

Total Ownership |

(Premium × 12) + OOP Max |

Total annual liability |

The table above demonstrates how to aggregate fixed and variable costs to determine your true financial exposure. This prevents the failure mode of “premium-only budgeting,” where a user assumes a $200 monthly plan is cheap, only to realize they owe a $5,000 deductible immediately upon a diagnosis.

Why low premiums can lead to financial insecurity

University Health Services notes that generally, the less expensive plans have more restrictions and provide less coverage. While a $50 monthly premium looks attractive, it often signals a plan with a very high deductible. If your deductible is set at 5% of your gross annual income—a threshold TIG Advisors recommends as a maximum—you may find yourself unable to afford even basic specialist visits without depleting your savings.

Can you use HSA/FSA accounts to offset high deductibles?

Yes, pairing a High-Deductible Health Plan (HDHP) with a Health Savings Account (HSA) offers a ‘triple tax advantage’: pre-tax contributions, tax-free growth, and tax-free distributions for qualified medical expenses. Unlike FSAs, which often follow ‘use-it-or-lose-it’ rules, HSA funds roll over indefinitely.

The Triple Tax Advantage Explained

This financial strategy works in three distinct stages. First, your contributions are made pre-tax to reduce taxable income. Next, any interest or investment growth within the account is tax-free. Finally, distributions used for qualified medical expenses are also tax-free.

For the 2025 plan year, McConkey reports that the minimum self-only deductible for HDHPs is $1,650, while the minimum family deductible is $3,300. Using an HSA to fund these high initial costs allows you to pay with “cheaper” dollars than your standard post-tax income.

Shortcut: To check your current HSA balance or contribution limits, log into your provider’s mobile app and navigate to > Accounts > HSA Details.

HSA vs. FSA: Portability and Rollover Rules

A common mistake is treating an FSA like an HSA. Shenandoah Dental Center points out that HSA funds roll over indefinitely and are portable, meaning you keep the money even if you change jobs. Conversely, FSAs often operate under “use-it-or-lose-it” rules, where unspent funds expire at the end of the plan year. This failure to use funds can result in losing hundreds of dollars in benefits.

What are the essential components of health insurance coverage?

Standard coverage includes 10 essential health benefits mandated by the ACA, such as preventive care, emergency services, hospitalization, mental health, and prescription drugs. Understanding your deductible (what you pay before insurance kicks in) and out-of-pocket maximum (your absolute spending limit) is critical for budgeting.

Defining Deductibles, Copays, and Out-of-Pocket Maximums

To navigate a plan effectively, you must distinguish between different cost-sharing mechanisms. TIG Advisors defines the deductible as the amount you pay out of pocket before your health insurance starts to cover costs. Once you have paid this amount, you move into the “coinsurance” phase, where the insurer pays a percentage of the bill.

Copayments are fixed amounts for specific services. For example, CMS provides an example copayment amount of $20 for a standard doctor’s visit. This is different from coinsurance, which is a percentage. University Health Services clarifies that once the out-of-pocket limit has been met, the plan will pay 100% of covered charges for the rest of that plan year.

The 10 Essential Health Benefits

According to Healthcare.gov, Marketplace plans are required to cover 10 essential health benefits. Anthem confirms that all ACA plans include coverage for these benefits to ensure a baseline of care. These benefits include:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative services and devices

- Laboratory services

- Preventive and wellness services

- Pediatric services, including oral and vision care

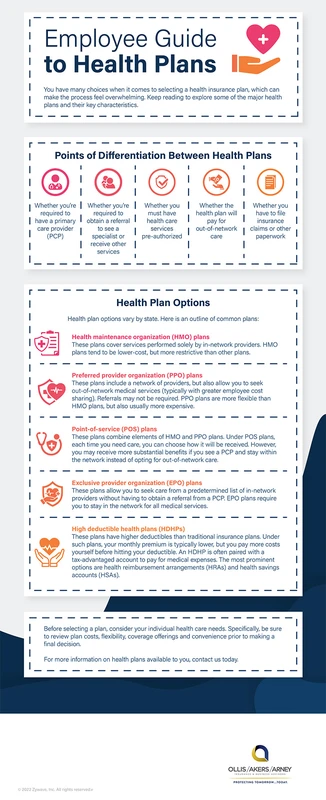

How do HMO and PPO networks impact your costs?

Network types dictate your access to doctors. HMOs typically require you to use a specific network and often require a referral from a Primary Care Provider (PCP) to see a specialist. PPOs offer more flexibility, allowing you to see specialists without a referral, though often at a higher premium.

Feature |

HMO (Health Maintenance Organization) |

PPO (Preferred Provider Organization) |

|---|---|---|

Specialist Referrals |

Often required from a PCP |

Not required |

Network Flexibility |

Limited to specific providers |

Higher; includes out-of-network options |

Out-of-Network Cost |

Generally not covered |

Covered, but at a higher cost |

Primary Care Requirement |

Usually mandatory |

Not mandatory |

The comparison above is based on data from Anthem and University Health Services regarding provider access. When choosing between these models, consider your existing relationship with your medical team.

HMO vs. PPO: A Comparison of Flexibility and Cost

Anthem notes that HMOs limit coverage to select care providers in the plan’s network. If you want to see a specialist, you may first need to visit your Primary Care Provider (PCP) to obtain a referral. In contrast, PPOs do not require a PCP referral to see a specialist, offering much greater freedom for those who want direct access to experts.

The Danger of Out-of-Network Care

Using in-network providers results in lower out-of-pocket costs, according to Anthem. If you visit a provider outside your plan’s network, you risk losing access to specific specialists and may be held responsible for the entire bill.

What common mistakes lead to denied insurance claims?

Claims are frequently rejected due to undisclosed medical history or failing to verify if a provider is in-network. Ignoring prescription drug tier restrictions can also trigger unexpected costs.

Warning: Never assume a doctor is covered. Always verify their status through official channels before booking an appointment to avoid massive unexpected bills.

The Disclosure Trap: Why Honesty Matters

TIG Advisors warns that insurance companies may review medical records later. If they find undisclosed information, they may reject claims for existing conditions, leaving you with the full financial burden of your treatment.

Prescription Tiers and Prior Authorizations

Medication costs are not uniform across all plans. HealthcareInsider.com recommends that you check which tier medications fall into and determine if prior authorization is required. Many plans use a tiered system where “Tier 1” drugs are low-cost generics and “Tier 4” drugs are expensive brand-name medications. If you do not obtain prior authorization for a high-tier drug, the claim will likely be denied.

Proactive Verification: Using Your Insurance App

To prevent claim denials, you must be proactive. University Health Services suggests three reliable methods for verifying networks: use the insurer’s official website, utilize their mobile app, or call the phone number located on the back of your insurance card. Checking these details before a procedure is the only way to ensure the “in-network” status is current and accurate.

FAQ

When is the health insurance Open Enrollment period?

The Marketplace Open Enrollment period typically runs from November 1 to January 15, according to Healthcare.gov. During this window, you can select or change your coverage for the upcoming year.

How can I check if my doctor is in my insurance network?

You can verify coverage by calling the phone number on the back of your insurance card, using the insurer’s website, or using their mobile app, as recommended by University Health Services.

What happens once I reach my out-of-pocket maximum?

Once the out-of-pocket limit has been met, the insurance plan will pay 100% of covered charges for the remainder of that plan year, according to University Health Services.

What is the difference between an FSA and an HSA?

HSAs offer triple tax advantages and funds roll over indefinitely, whereas FSAs often follow “use-it-or-lose-it” rules where funds may expire if not used by year-end, per Shenandoah Dental Center.

Advertisement