Advertisement

CRM FanzineFaves – Deciding between individual and family coverage involves weighing household size against total premium costs. While individual plans offer separate coverage, a family of four can save approximately $883 per month by utilizing a single family plan instead of purchasing four separate individual plans (Source: Venteur, 2026 projections).

A family of four can save approximately $883 per month by utilizing a single family plan instead of purchasing four separate individual plans (Source: Venteur, 2026 projections).

How do embedded vs. aggregate deductibles impact your family’s finances?

The difference depends on whether you use an embedded or aggregate structure. An embedded deductible applies an individual limit to each person, while an aggregate deductible requires the entire family’s combined spending to reach a specific threshold before the insurer pays.

Advertisement

Many policyholders assume that once any family member hits a certain spending mark, the insurance starts paying for everyone. This is a dangerous misconception. If you select an aggregate deductible plan, a single medical event for one child might not trigger insurance coverage until the entire family’s combined expenses meet a massive, multi-thousand-dollar threshold.

The ‘Shared Sum’ Risk: When one member exhausts the limit

In an embedded deductible structure, the plan provides a “safety net” for individuals. For example, if the family deductible is $6,000 but the embedded individual limit is $3,000, a single person’s surgery that costs $4,000 will trigger coverage for the remaining $1,000 after they hit their $3,000 limit. This prevents a single illness from draining the entire family’s liquid assets before the insurer contributes a single cent.

Why aggregate deductibles can lead to financial surprises

Aggregate plans are often marketed as having lower monthly premiums, but they fail when a single high-utilizer is present in the household. I have observed cases where a parent chooses an aggregate plan to save $50 per month, only to be hit with a $12,000 bill because the family’s total spending had not yet reached the aggregate threshold. This is a mathematical trap that ignores the volatility of individual health needs.

Which plan is better for life transitions like divorce or aging out?

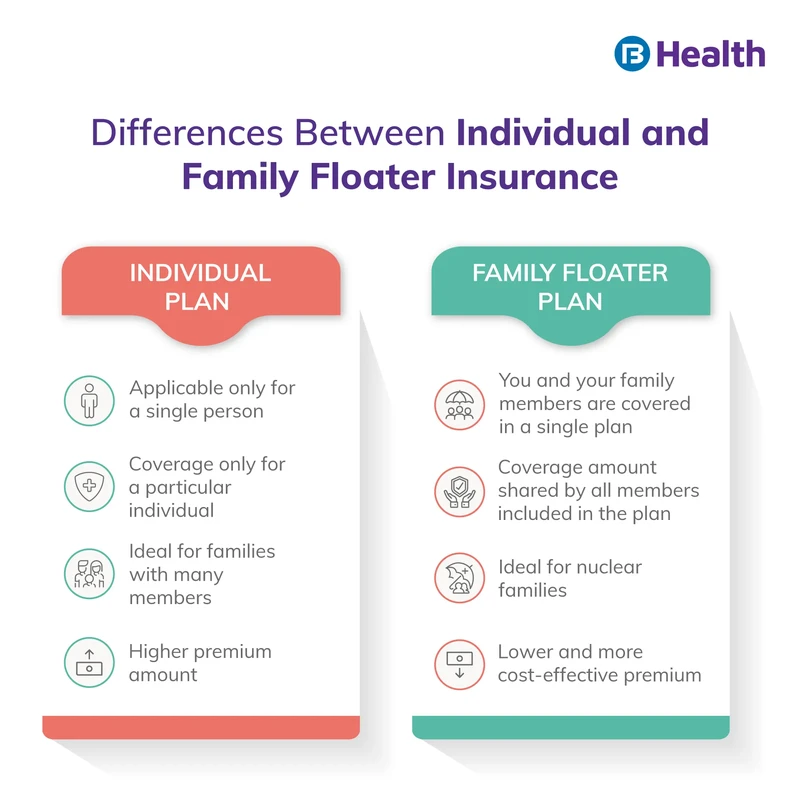

When transitioning from family to individual coverage—such as when a child turns 26 or during a divorce—you must pivot to individual plans to avoid coverage gaps. Individual plans offer separate safety nets, whereas family plans are tied to the oldest member’s age and health profile.

To avoid denied claims for medications or specialist visits, you must manage your marketplace status carefully. For example, children can typically remain on a family plan until age 26, according to Blue Shield of CA, but must secure their own individual policy once they hit this limit.

- The Age 26 Rule: Children can typically remain on a family plan until age 26, according to Blue Shield of CA. Once they hit this limit, they must secure their own individual policy.

- Divorce or Legal Separation: A change in household composition requires a Special Enrollment Period to move from a joint family plan to separate individual plans.

- Marriage: Adding a spouse to an existing plan is a qualifying life event that allows for mid-year plan adjustments.

The Age 26 Rule: Transitioning dependents

The transition at age 26 is a hard boundary. While some premium exception rules might exist for those aged 21 in specific niche contexts, the standard federal limit remains 26. When a child “ages out,” they essentially become a new individual consumer in the insurance marketplace, often facing higher premiums due to their individual age profile compared to being a dependent.

Managing the ‘Split Household’ administrative burden

Managing separate individual plans after a divorce creates significant overhead. You must track different Explanation of Benefits (EOB) documents, manage separate login credentials for providers like Anthem or BCBS, and monitor different renewal dates. This administrative friction is a direct trade-off for the flexibility of having independent coverage that is not tied to an ex-spouse’s health status or premium changes.

Is a family plan actually cheaper per person?

Yes, mathematically. While total premiums for a family plan are higher (averaging $1,437/month in 2026), the cost per person is significantly lower for households with 3 or more members compared to buying individual marketplace plans.

To evaluate affordability, compare the “per capita” cost against individual marketplace rates. For instance, a single adult (age 30) faces an average premium of $638, but a family plan distributes the total cost across all members.

Household Size |

Plan Type |

Avg. Monthly Premium |

Est. Cost Per Person |

|---|---|---|---|

1 Adult (Age 30) |

Individual |

$638 |

$638 |

2 Adults (Age 30) |

Couple |

$1,276 |

$638 |

1 Adult + 1 Child |

Family |

$958 |

$479 |

Family of 4 |

Family |

$2,320 |

$580 |

Family of 4 (Parents 40) |

Family |

$2,256 |

$564 |

The data above shows that even with aging parents, the per-person cost of a family plan remains lower than the $638 average for a single 30-year-old. For a family of four, choosing individual plans for everyone would cost approximately $2,320 per month, whereas a single family plan can offer substantial savings.

2026 Cost Projections: Individual vs. Family

For a single adult, the average marketplace premium is projected at $752 for 2026. However, if you are a healthy individual, you might find costs as low as $139 per month, or between $225 and $327 for standard plans. The math changes drastically once you add dependents, as family premiums are generally calculated based on the age and health of the oldest member of the family.

The ‘Break-Even’ Formula for 3+ Person Households

To determine if a family plan is the right move, use this logic: Divide the total family premium by the number of covered members. If this number is lower than the cost of the individual plans you would otherwise purchase, the family plan is the winner. For a family of four, the $883 monthly savings identified by Venteur makes the family plan the obvious mathematical choice.

How do Gold, Silver, and Bronze tiers affect your out-of-pocket costs?

Plan tiers balance monthly premiums against care costs. Gold plans have the highest premiums but cover ~80% of costs, whereas Bronze plans have the lowest premiums but require you to pay ~40% of care costs.

As HealthPartners notes, “Generally, the higher your premium, the lower your out-of-pocket costs.” You must decide if you prefer paying more monthly to receive higher coverage percentages from your insurer.

Plan Tier |

Premium Level |

Insurer Pays |

You Pay |

|---|---|---|---|

Gold |

Highest |

~80% |

~20% |

Silver |

Moderate |

~70% |

~30% |

Bronze |

Lowest |

~60% |

~40% |

The table above compares the coverage ratios for each tier. For example, in a Gold plan, the insurer covers approximately 80% of costs, while in a Bronze plan, the insurer covers approximately 60%.

The Silver Plan Advantage: Cost-Sharing Reductions (CSR)

Silver plans possess a unique feature: Cost-Sharing Reductions (CSR). A CSR is a discount that lowers costs for copayments, coinsurance, and deductibles. This benefit is available only with silver-level plans on the marketplace. If your income falls within certain limits, a Silver plan can effectively function like a Gold plan by significantly lowering your out-of-pocket maximums.

Choosing between HMO and PPO networks

When selecting a tier, you must also consider the network type. An HMO (Health Maintenance Organization) typically requires you to stay within a specific network and get referrals, while a PPO (Preferred Provider Organization) offers more flexibility. This choice is critical because a Gold PPO plan might still be more expensive than a Silver HMO if you frequently see out-of-network specialists.

Can you use an HSA to offset individual or family costs?

Health Savings Accounts (HSAs) allow you to save for medical expenses with triple tax benefits. In 2025, individuals can contribute up to $4,300, while families can contribute up to $8,550, with additional catch-up amounts for those 55+.

By pairing a Bronze or Silver HDHP with an HSA, you can mitigate the high out-of-pocket costs associated with lower-tier plans. Unlike Flexible Spending Accounts (FSAs), which have a “use-it-or-lose-it” policy, HSAs allow unused funds to roll over annually.

Shortcut: To check your HSA contribution eligibility, navigate to your insurance provider’s portal: BCBS Portal > My Account > Benefits Summary.

HSA vs. FSA: The rollover advantage

The primary failure mode in medical savings is the “use-it-or-lose-it” trap of the FSA. If you miscalculate your medical needs and have $500 left in an FSA at the end of the year, that money is gone. In contrast, HSA funds belong to you indefinitely. This makes the HSA a superior vehicle for long-term wealth building and managing healthcare costs as you age toward Medicare eligibility at age 65.

Maximizing contributions for 2025

To maximize your benefits, you should aim to hit the IRS limits. For 2025, ensure you do not exceed the $4,300 limit for individual plans or the $8,550 limit for families. If you are aged 55 or older, you can contribute an additional $1,000 as a catch-up amount. This is a critical way to lower your taxable income while building a dedicated fund for future medical expenses.

FAQ

At what age can children be removed from a family plan?

Children can typically remain on a family plan until age 26, according to Blue Shield of CA. Once they reach this age, they are generally required to transition to their own individual coverage unless they meet specific disability requirements.

Is Medicare an option for families?

No, Medicare is only available to individuals, whereas Medicaid can cover both individuals and families. Medicare eligibility typically begins when an individual reaches 65 years of age.

How are family premiums calculated?

Family health insurance premiums are generally calculated based on the age and health of the oldest member of the family. This means the age of the oldest adult has a disproportionate impact on the total monthly cost.

Advertisement