Advertisement

CRM FanzineFaves – A car insurance premium is the specific amount of money you pay an insurance company to provide financial protection for yourself and your vehicle. While average U.S. costs reached $2,697 per year by May 2026, your individual rate is determined by a unique formula involving risk assessment, driving history, and vehicle type.

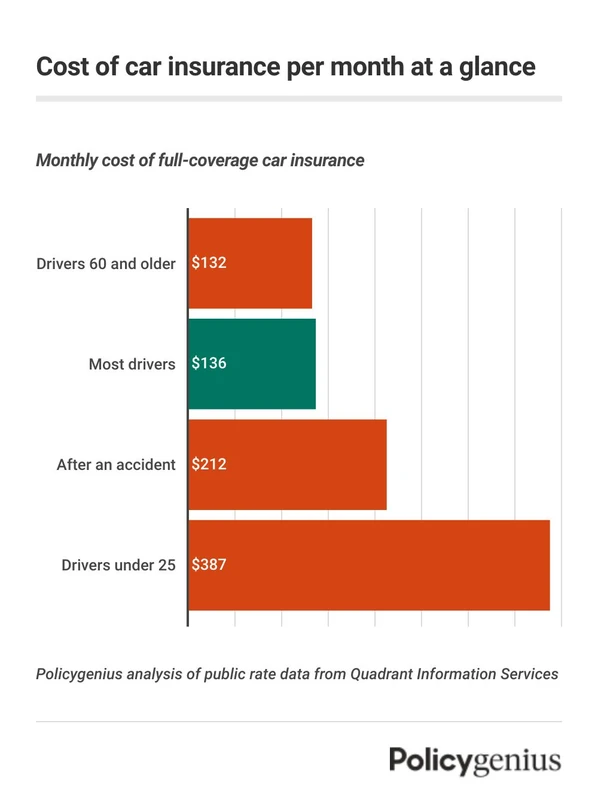

The average cost of car insurance in the U.S. reached $2,697 per year as of May 2026, representing a 12% increase in full coverage costs since 2024.

Why do car insurance premiums fluctuate? The ‘Volatility Index’ explained.

Premiums fluctuate due to both personal behavior and macroeconomic shifts. Key drivers include rising costs for auto parts and labor, increased accident rates in specific ZIP codes, and even national tariffs on imported vehicles, which can drive up the cost of property damage and collision coverage.

Advertisement

External economic pressures frequently override individual driving habits. Rises in auto parts and labor can drive up the cost of property damage liability, collision and comprehensive coverage. When repair shops charge more for specialized technician time, insurers must raise premiums to cover these higher claim payouts. In 2022, the auto industry paid out $1.12 for every $1.00 collected in premiums, signaling a significant imbalance in cost recovery.

The impact of the 25% vehicle tariff

Macroeconomic policy directly influences your monthly bill. On April 3, 2025, the U.S. imposed a 25 percent tariff on all imported passenger vehicles. This policy, combined with a tariff against automotive parts that took effect on May 3, 2025, increases the replacement value of many vehicles. Because insurers must cover the cost of replacing or repairing damaged cars, these tariffs effectively raise the baseline for collision and comprehensive coverage rates across the country.

How ZIP code accident rates affect your renewal

Your location acts as a proxy for risk. An increase in accidents in a specific ZIP code can increase premiums even without a personal claim. Insurers use Risk Assessment Sorting to group drivers by geography; if your neighborhood experiences a surge in fender benders or theft, the entire local pool faces higher costs. This can lead to “renewal shock” where your rate jumps despite your own safe driving behavior.

Telematics vs. Traditional: Can driving apps actually lower your rates?

Telematics (Usage-Based Insurance) shifts your premium from a demographic-based model to a behavior-based model. By using technology to monitor speeding and braking, drivers can achieve significant savings—up to 15% in some cases—by proving they are low-risk through actual driving data.

Traditional insurance relies on static data like age and gender. In contrast, Telematics / Usage-Based Insurance (UBI) utilizes real-time data to reward safer habits. For example, XYZ Logistics saw a 15 percent decrease in insurance premiums after implementing telematics systems within their fleet. This shift proves that measurable data is more accurate than historical demographic averages.

Improved driver behavior, such as reduced speeding and harsh braking, translates to safer driving. This, in turn, lowers the likelihood of accidents and contributes to lower insurance premiums. To utilize this, many drivers follow a path similar to: Mobile App > Settings > Telematics Enrollment.

- Speeding: Monitoring how often a driver exceeds posted limits.

- Braking: Tracking “harsh braking” events that indicate distracted or aggressive driving.

- Time of Day: Assessing risk based on late-night driving patterns.

- Mileage: Adjusting rates for low-mileage commuters.

Technical interruptions can impact your score. If a driver’s phone battery dies or a GPS signal is lost, it creates data gaps. These “dark periods” may cause insurers to view the driver as a higher risk.

What are the primary factors that determine your premium?

Insurance companies use unique formulas to calculate premiums based on risk assessment. The most significant factors include your driving history, credit score (which correlates with claim frequency), vehicle type, location, and the level of coverage you select, such as full vs. minimum coverage.

Underwriters do not use a one-size-fits-all approach. Instead, they utilize Risk Assessment Sorting to categorize drivers into specific risk tiers. While many assume only accidents matter, the underlying math is far more complex. For instance, the Texas Department of Insurance notes that “The premium is the rate ($3.50) times the unit (14 gallons),” illustrating how specific variables are multiplied to reach a final cost.

Factor |

Impact on Premium |

Reasoning |

|---|---|---|

Driving History |

High |

Accidents and tickets increase risk profile. |

Credit Score |

Medium/High |

Poor scores correlate with higher claim frequency. |

Vehicle Type |

Medium |

Safety tech and repair costs vary by model. |

Location (ZIP) |

High |

Local accident and theft rates affect rates. |

Coverage Level |

Variable |

Full coverage costs more than minimum. |

Risk Assessment Sorting allows insurers to group drivers by age, location, and profile to determine a base rate before adjusting for specific vehicle history.

The role of credit scores in underwriting

A counterintuitive reality of the insurance industry is the link between financial management and driving risk. Insurance companies point to numerous studies that correlate poor credit scores with higher numbers of claims. Because creditworthiness is often used as a predictor of general responsibility, a lower score can lead to significantly higher premiums even if your driving record is spotless.

How vehicle safety tech affects repair costs

Modern vehicles are essentially computers on wheels. While advanced driver-assistance systems (ADAS) are designed to prevent accidents, they can paradoxically increase premiums. If a sensor in a bumper is damaged, the cost to recalibrate the software and replace the hardware is substantially higher than a traditional metal bumper repair. This complexity drives up the “total loss” threshold for many modern cars.

How can you lower your car insurance premium?

You can reduce premiums by increasing your deductibles, paying your policy in full rather than monthly, and shopping around for multiple quotes. Comparing rates can lead to potential savings of up to 30% depending on the provider and coverage type.

One reliable method to lower costs is Deductible Adjustment. By opting for higher collision and comprehensive deductibles, you assume more of the initial risk, which lowers the insurer’s liability and, consequently, your premium. This strategy works best if you maintain an emergency fund to cover the higher out-of-pocket cost during a claim.

Shortcut: To quickly find ways to save, log into your provider’s portal and navigate to Policy Management > Discounts & Credits to see if you qualify for multi-policy or safe-driver discounts.

The math of higher deductibles

Increasing a deductible from $500 to $1,000 might seem risky, but the math often favors the consumer. If your annual premium drops by $200 due to the higher deductible, it would take five years of no accidents to “break even” on that $500 difference. For many drivers, this is a statistically sound trade-off.

The ‘Pay in Full’ advantage

Most insurers offer a financial incentive for immediate payment. According to The Hartford, paying in full often results in a discount. This is a simple way to avoid the administrative costs and interest-like fees associated with monthly installment plans. If you have the liquidity, paying the entire term upfront is almost always the cheaper option.

What are the most common premium pitfalls to avoid?

Failing to disclose prior accidents can lead to much higher premiums than quoted. Additionally, drivers often face “renewal shock” when insurers re-evaluate risk at the end of a 6 or 12-month term.

Transparency is vital during the application process. Many drivers believe that small “fender benders” don’t need to be reported, but this is a dangerous misconception. As Progressive warns, “If you don’t disclose prior accidents you were involved in, your car insurance premium could be significantly higher than the quoted amount.” This discrepancy usually surfaces during the underwriting audit, leading to policy cancellation or retroactive rate hikes.

The danger of non-disclosure

Non-disclosure is a major risk factor. If an insurer discovers an undisclosed accident during a claim investigation, they may deny the claim entirely. This leaves you personally liable for all damages.

Managing renewal-period rate hikes

Premium stability breaks at the end of a policy term during renewal. This is when insurers re-evaluate your risk, check for new accidents, and adjust for inflation. To avoid being caught off guard, you should treat the renewal period as a new shopping window. Low premium rates break when a driver accumulates multiple speeding tickets or at-fault accidents within a short period, making it essential to review your coverage every 6 to 12 months.

FAQ

According to recent data, minimum coverage averages between $621 and $820 per year, depending on the provider and region. These rates vary significantly based on the state’s legal requirements and the specific insurer’s risk model.

Advertisement

Advertisement