Advertisement

CRM FanzineFaves – Third-party insurance covers legal liability for damages you cause to others, whereas comprehensive insurance covers both third-party liability and damages to your own vehicle, including theft, fire, and weather. While third-party is often a legal minimum, comprehensive provides a ‘superhero cape’ of protection against personal financial exposure.

Comprehensive premiums generally run 3 to 5 times higher than third-party premiums, but the difference is not about legality; it is about financial exposure.

Is Third-Party Insurance Enough to Protect Your Personal Assets?

Third-party insurance only covers the other party’s damages. If a lawsuit exceeds your policy limits—such as the $250,000 or $500,000 limits seen in Michigan—you are personally liable for the remaining balance, potentially risking your savings, home, and future earnings.

Advertisement

A LinkedIn Article notes that “The difference is not about legality. It is about financial exposure.” If you are involved in a serious accident, the costs can escalate far beyond basic policy caps.

The ‘Maximum Limit’ Trap

Legal mandates often set floors rather than ceilings for protection. For example, Michigan auto law established specific minimums that took effect in July 2020. Under these regulations, the minimum coverage limit for bodily injury to or death of 1 person in any 1 accident is $250,000. If the accident involves 2 or more persons, that minimum requirement rises to $500,000.

Relying solely on these numbers creates a dangerous ceiling. If a court awards a victim $750,000 following a collision, your $500,000 policy leaves a $250,000 deficit. This gap is not covered by your insurer, meaning you must pay the difference out of your own pocket.

The Financial Ruin Scenario: Liability vs. Personal Assets

If a driver with only third-party coverage causes a multi-car accident, they face significant personal risk once the policy limit is reached. For instance, if a driver’s policy is capped at the Michigan minimum of $500,000 for multiple persons, any damages exceeding that amount become the driver’s direct responsibility.

How Do I Know When to Switch from Comprehensive to Third-Party?

Use the ‘Quote-to-Value Ratio’ to decide. Calculate your annual premium divided by the car’s current market value. If the ratio exceeds 5%, or if your vehicle’s value is near the $3,000 ‘runabout’ threshold, switching to third-party may be more cost-effective.

National Cover Insurance recommends using the “Quote-to-Value Ratio” technique to ensure you are not overpaying for protection on a depreciating asset.

Shortcut: To perform a quick audit, divide your annual premium by your car’s current market value. If the result is higher than 0.05 (5%), your comprehensive coverage may be costing more than the vehicle is worth.

The Depreciation vs. Premium Audit

Vehicles lose value every year, but insurance premiums do not always drop at the same rate. If you own a vehicle valued at $3,000, which is the threshold for a “runabout” vehicle according to National Cover Insurance, paying a high comprehensive premium might be a poor financial move. In these cases, the cost of the insurance starts to rival the cost of replacing the car itself.

The Tipping Point: When your car is worth less than the risk

The tipping point occurs when the total cost of premiums over a 2-year period approaches the total market value of the car. While comprehensive insurance is better for newer or expensive cars, an old vehicle that is frequently parked in a secure garage might not justify the high cost of comprehensive coverage. However, this strategy breaks when you live in a high-theft area or a region prone to extreme weather.

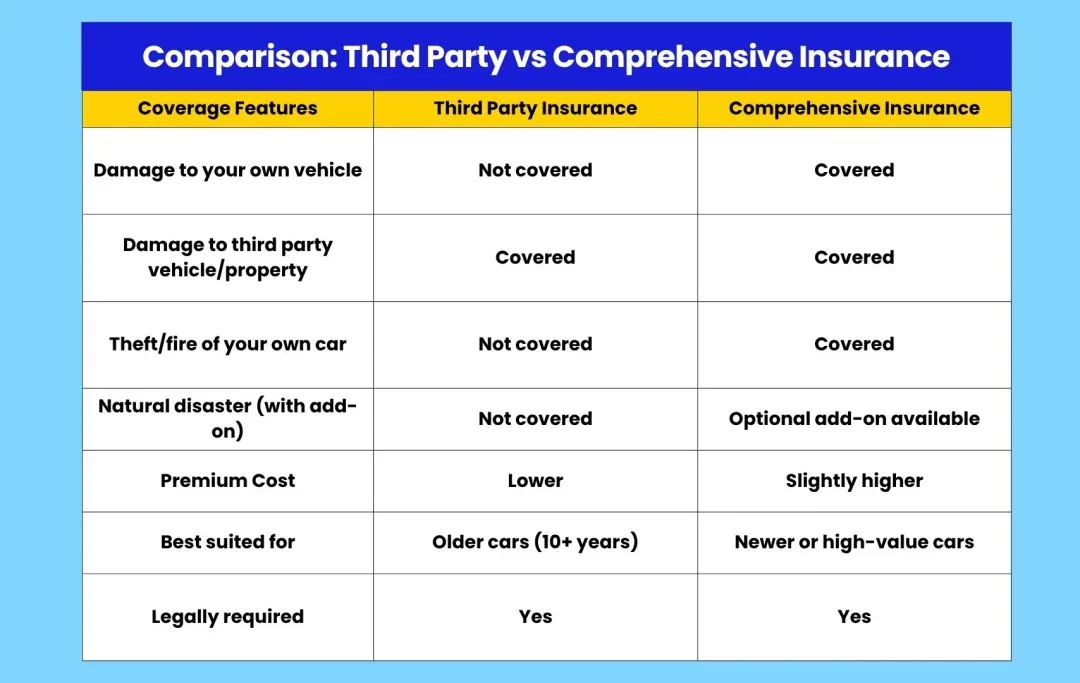

What are the Core Differences in Coverage Scope?

According to Pineapple, comprehensive insurance is the “all-in-one” option that covers theft, accidental damage, fire, and weather-related losses. In contrast, third-party insurance is strictly limited to liability for others and does not cover damage to your own vehicle or theft.

Mathapelo Mosia from Pineapple describes Comprehensive Insurance as the “all-in-one” option—covering everything from theft to accidental damage. She compares it to “having a superhero cape for your car.” Conversely, third-party insurance is a much narrower tool designed only to satisfy legal requirements for external damages.

Feature |

Third-Party Insurance |

Comprehensive Insurance |

|---|---|---|

Third-Party Liability |

Included |

Included |

Theft & Fire Protection |

Not Covered |

Included |

Weather/Storm Damage |

Not Covered |

Included |

Own Vehicle Damage |

Not Covered |

Included |

Best For |

Low-value/Old vehicles |

Newer/Expensive vehicles |

Leadway Assurance Company Limited notes that comprehensive insurance is better than third-party insurance as it provides coverage for a wide variety of damages, injuries, and losses.

The ‘Middle Ground’: Third-Party, Fire & Theft

Some drivers opt for a hybrid approach known as Third-Party, Fire, and Theft (TPFT). This provides more protection than basic liability but lacks the “all-in-one” nature of comprehensive. For instance, NRMA Insurance notes that Third-Party Property Damage (TPPD) specifically does not cover hail or storm damage, which is a critical distinction for drivers in volatile climates.

Loss of Use: Why temporary transportation matters

A major hidden cost of accidents is the loss of mobility. According to Goodrates Insurance Ontario, some comprehensive policies include “Loss of Use” coverage. This pays for temporary transportation, such as renting a car or taking a taxi, while your vehicle is undergoing repairs. Third-party insurance offers zero compensation for this inconvenience, leaving you to fund your own travel during the repair period.

Why Do Lenders Mandate Comprehensive Insurance?

If you lease or finance a vehicle, lenders require comprehensive insurance to protect their collateral. If the car is totaled, comprehensive insurance ensures the loan is covered, whereas third-party would leave you owing the full balance without a car.

Lenders view your vehicle as collateral for the debt you owe. If a car is stolen or destroyed in a fire, a third-party policy provides no funds to replace the asset. This creates a massive risk for the bank, which is why they mandate comprehensive coverage as a condition of the loan agreement.

Lease & Loan Compliance Guide

IronRock Insurance points out that having a comprehensive policy significantly reduces your out-of-pocket costs if you are at fault in an accident. This helps you maintain your ability to continue making loan payments despite the damage.

The Gap Insurance Connection

For many, comprehensive insurance is just the first step. Because cars depreciate quickly, the insurance payout might be less than the remaining loan balance. This is where the interaction between comprehensive coverage and the car’s actual cash value becomes critical. If you are driving a relatively new or expensive car, Leadway Assurance recommends maximum protection to mitigate these financial gaps.

How Can I Avoid Common Insurance Claim Denials?

To prevent claim denial, ensure all personal details (name, DOB) match insurer records, disclose all pre-existing vehicle conditions before signing, and never over-report a vehicle’s value to lower premiums, as this constitutes insurance fraud.

To ensure your claim is processed smoothly, avoid common pitfalls such as undisclosed pre-existing conditions or incorrect personal data. Following these steps can prevent the administrative errors that lead to denials.

- Verify Personal Data: Ensure your name and Date of Birth (DOB) are spelled exactly as they appear on your government ID. Even a small typo can trigger a denial during the verification process.

- Disclose Pre-existing Conditions: If your vehicle already has a dent or a mechanical issue, disclose it before signing the policy. Failure to do so allows insurers to claim the damage was pre-existing.

- Avoid Value Inflation: Never report a higher car value than its actual worth to try and manipulate premium structures; this is considered insurance fraud and will void your coverage.

- Update Policy Details: If you move or change your primary vehicle usage, notify your provider immediately to ensure your coverage remains valid.

The ‘Incorrect Information’ Trap

Claim denials often occur when details like your name or Date of Birth (DOB) do not match the insurer’s database. This discrepancy can flag a policy as invalid during the verification stage of a claim.

The Truth About Over-Insuring Your Vehicle

In the event of a total loss, insurers will only pay the actual cash value of the vehicle. Reporting a value significantly higher than the market rate results in overpaying for coverage you can never actually collect.

FAQ

Is third-party insurance legally required?

Yes, third-party insurance is mandatory to cover liability to others. In Michigan, for example, specific minimums must be met to operate legally on public roads.

Does comprehensive insurance cover my rental car while mine is being repaired?

According to Goodrates Insurance Ontario, some comprehensive policies include “Loss of Use” coverage. This specific benefit pays for temporary transportation, such as renting a car or taking a taxi, while your vehicle is undergoing repairs.

Can I add specific protections to my comprehensive policy?

Yes, you can often customize policies with add-ons like zero-depreciation, engine protection, or gearbox coverage. These features allow you to tailor the “all-in-one” coverage to your specific vehicle’s needs and your driving habits.

Advertisement